In the last months of 2020 the international landscape of commitments to decarbonise the global economy and to combat climate change has rapidly changed. Following the European commitment of “climate neutrality” by 2050 and a 55% reduction in emissions by 2030, China pledged to achieve “carbon neutrality” before 2060 with “peak emissions” before 2030, and President Biden announced the US commitment for carbon-free electricity sector by 2035 and carbon neutrality by 2050. Japan, UK, South Korea, Canada share the same commitments, while India planned to achieve around 60% of its installed electricity generation capacity from renewables and clean sources by 2030 as the first step towards decarbonisation.

In other words the major economies of the planet have made unilateral and unconditional commitments to zero carbon emissions within the next 30-40 years, and the international reference framework of the without-end COPs negotiations has drastically changed.

Today the focus of large economies shifts from the search for the most suitable “wording” to certify the stalemate in negotiations on climate change to the feasibility of the convergence on global scale of the policies and measures to drive the “inertial turn” (industrial, technological and economic) necessary to the progressive phase out of fossil fuels.

The decade that has just begun will be decisive, because achieving the 2030-2035 objectives requires not only the growth of alternative zero-emission sources in the energy portfolio of the economies, but also the building and management of efficient systems for optimizing the use and worldwide access to clean energies.

What are the available technological and industrial options that can now start the no return path of decarbonization within 2030-2035 ? As for the availability of zero carbon emission sources and technologies able to meet the 2030-2035 targets, today nuclear energy, hydrogen and renewables must be considered.

Nuclear Energy

Nuclear energy is today the second low-carbon source of electricity.

According to the International Energy Agency “Sustainable Development Scenario”, fully aligned with the Paris Agreement, an average of 15 GW of new nuclear capacity is required annually between 2020 and 2040 ( Nuclear Power- tracking report- June 2020).

Nevertheless, the data show that the construction of new plants is far below the objectives of the SDS, while the decommissioning of existing plants continues mainly due to the post-Fukushima in Japan and to the energy policies in Europe (Germany, Sweden, Switzerland) or to high management costs (US).

In 2019 and 2020, the new installed nuclear capacity is lower than the decommissioned one. It should also be noted that the refurbishment of existing plants further reduces the contribution of nuclear energy to electricity production in the short term.

The long times required to build and bring new nuclear energy facilities into commercial operation should also be underlined.

In the 2030-2035 horizon, nuclear energy will therefore not make a significant contribution to decarbonization, while in the medium to long term a more effective contribution is expected by new plants in China, Russia, USA, India, Korea, UK, United Arab Emirates.

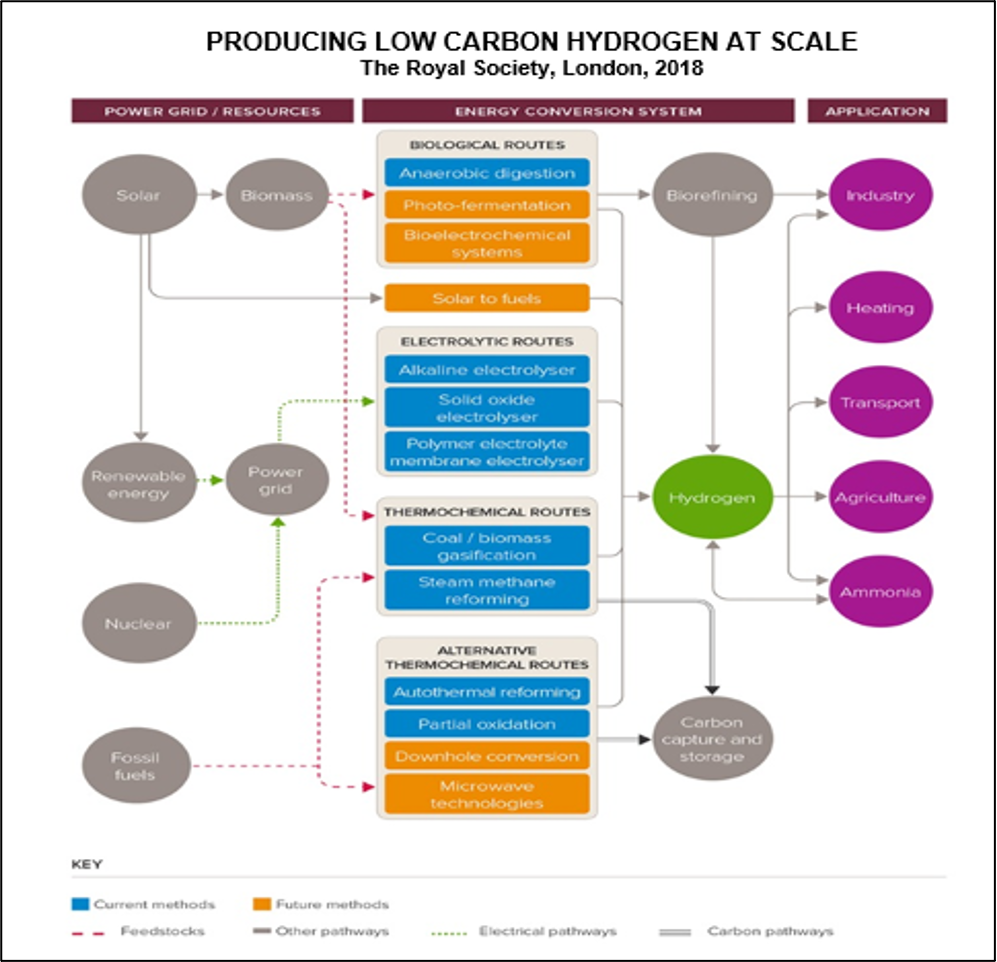

Hydrogen

Hydrogen is an energy carrier that can be used to store, move, and deliver energy.

Hydrogen can be produced from natural gas, coal and other fossil fuels, water and biomass.

Today the primary uses of hydrogen are in the oil refineries and chemical industries, and about 95% of all hydrogen is produced from fossil fuels (mostly steam reforming of natural gas). “As a consequence, production of hydrogen is responsible for annual CO2 emissions equivalent to those of Indonesia and the United Kingdom combined”. (The future of Hydrogen- International Energy Agency).

Nevertheless, hydrogen is becoming a flagship of green energy transition.

There are two drivers of the hydrogen environmental appeal and enthusiasm :

- hydrogen fuel cells vehicles and power/heat production plants fueled by hydrogen emit clean water;

- hydrogen can store energy for days, weeks or months, and can be used in power generation as well as in energy transportation over long distances through the existing natural gas pipelines.

But as long as the production of hydrogen is a source of carbon emissions, it is clear that hydrogen cannot be the “key” to the energy transition in the short term.

Zero- carbon hydrogen, or green hydrogen, can be produced from water via electrolysis supplied by zero-carbon electricity, from either renewable or nuclear energy.

However, this necessary option towards a clean energy future requires medium to long times. According to the IEA report The Future of Hydrogen, “producing all of today’s dedicated hydrogen output from electricity would result in an electricity demand of 3.600 TWh, more than the total annual electricity generation of the European Union”.

Furthermore, green hydrogen cost is today more than double that of bleu hydrogen. Many analyzes agree that green hydrogen will be competitive with the cost of blue hydrogen no earlier than 2030, as a result of decreasing costs of renewables and electrolysers, as well as of the increasing renewable energy production.

A parallel option, very much supported by the major energy companies, is the production of bleu hydrogen from reforming of natural gas associated to Carbon Capture, Utilization and Storage (CCUS).

Without considering the costs and despite the fact that at least 20 plants are already in operation and another 10 are under construction, the technological solutions for these plants are still in an experimental phase. It should also be considered that the parallel development of green hydrogen could make the role of natural gas marginal in 10-15 years and the CCUS plants not economically sustainable.

In short, hydrogen will be a ready and widespread solution in the next decade.

Renewable Energies

The role of renewable energy grows as well as both the reduction of costs and the development of new technologies and new materials, with increasingly higher yields in solar and wind power.

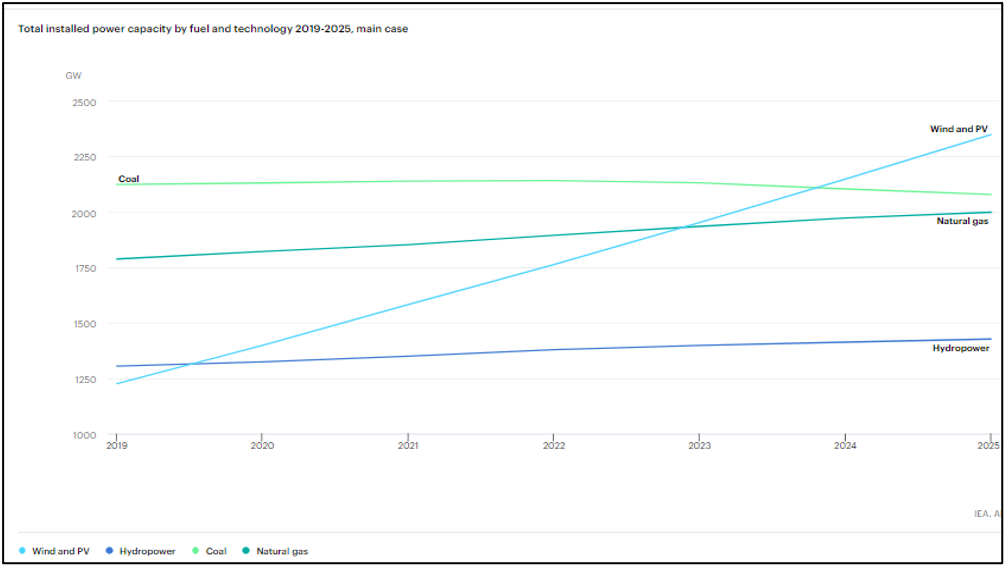

According to the Report of International Energy Agency, “Renewables 2020 Analysis and forecast to 2025” (November 2020), the total installed wind and solar PV capacity is on track to overtake natural gas in 2023 and coal in 2024. Overall, the generation from all renewable resources will become the “largest source of electricity generation worldwide in 2025,” supplying one-third of global power output and accounting for 95% of the increase in total power capacity through 2025.

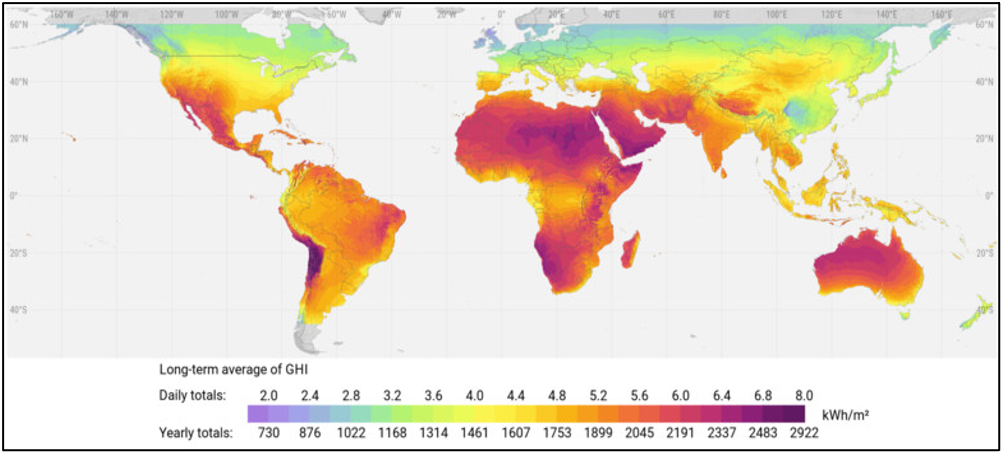

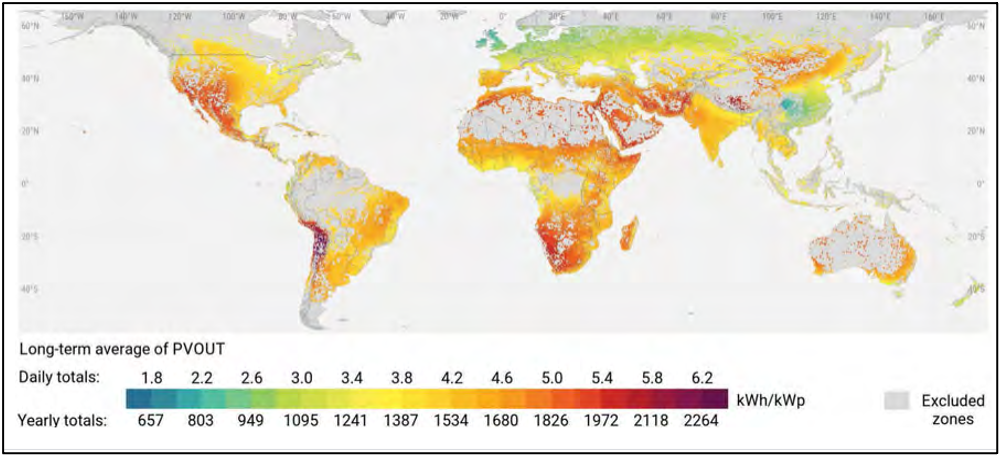

The grow potential of renewables is well represented by Global Solar Atlas released in December 2020 by World Bank Group- Energy Sector Management Assistance Program (ESMAP) and by the Global Wind Atlas released by the Technical University of Denmark (DTU) in partnership with the World Bank Group-ESMAP.

Solar Energy

The solar PV annual market could reach about 150 GW – an increase of almost 40%- in just three years (IEA, 2020 Renewables).

The theoretical potential is immense: it is estimated that the solar energy available annually is in a range between 1500 and about 50,000 exajoules (EJ). If we consider that world energy consumption is about 590 EJ, the use of the potential of solar radiation would be able to make energy available that is far greater than the current global demand and the expected increasing consumption in the coming decades.

The map of the potential of global horizontal solar irradiation (GHI), measured in kilowatthours per square meter (kWh / m2), offers a very clear picture of the “wells” of solar energy in the different regions of the planet.

Based on GHI, and taking into account the physical / technical constraints to the installation of PV modules, the Practical Photovoltaic Power Potential (measured in kilowatthours per installed kilowatt-peak of the system capacity -kWh/kWp) has been calculated. Around 20% of the global population lives in 70 countries boasting excellent conditions for PV, average exceeds 4.5 kWh/kWp per day, while countries in the favorable mid-range between 3.5 and 4.5 kWh/kWp account for 71% of the global population.

The data show that solar energy can respond widely to the global demand, and highlight that the highest potential is largely located in areas distant from the centers of consumption.

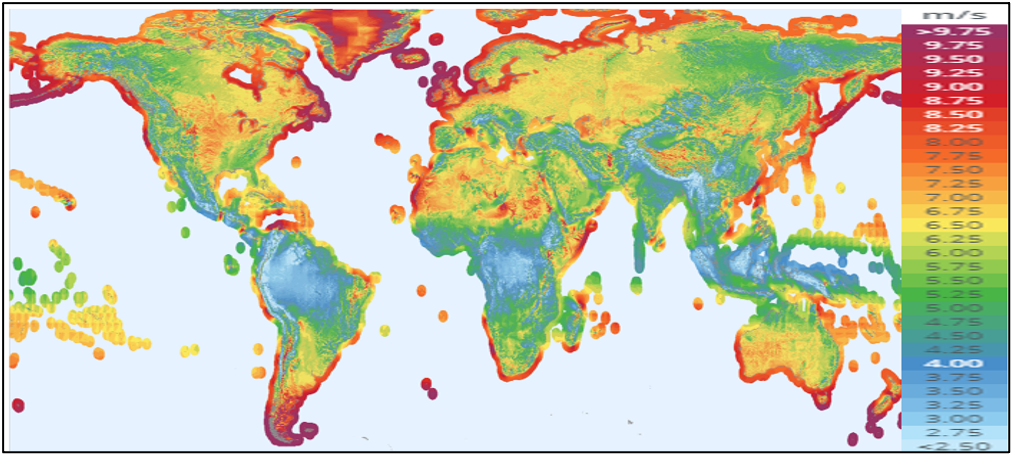

Wind Energy

The Global Wind Energy Council expects that over 355GW of new capacity will be added between 020-2024, hat is nearly 71GW of new installations each year until 2024.

The IEA report, “Renewables 2020 Analysis and forecast to 2025” estimates that annual global wind additions in 2023-25 could range from 65 GW in the main case and 100 GW in the accelerated case.

But the potential is much much higher.

The Global Wind Atlas highlights the on-shore and off-shore potential of wind power in all the regions, with the highest potentials often concentrated in remote and low-demand area on the coasts and seas of northern Europe, Canada, the Arctic region, southern Latin America, southern Africa, Australia.

According to many estimates, the potential of wind power is more than 40 times current worldwide consumption of electricity, and more than 5 times total global use of energy.

Solar&Wind competitiveness

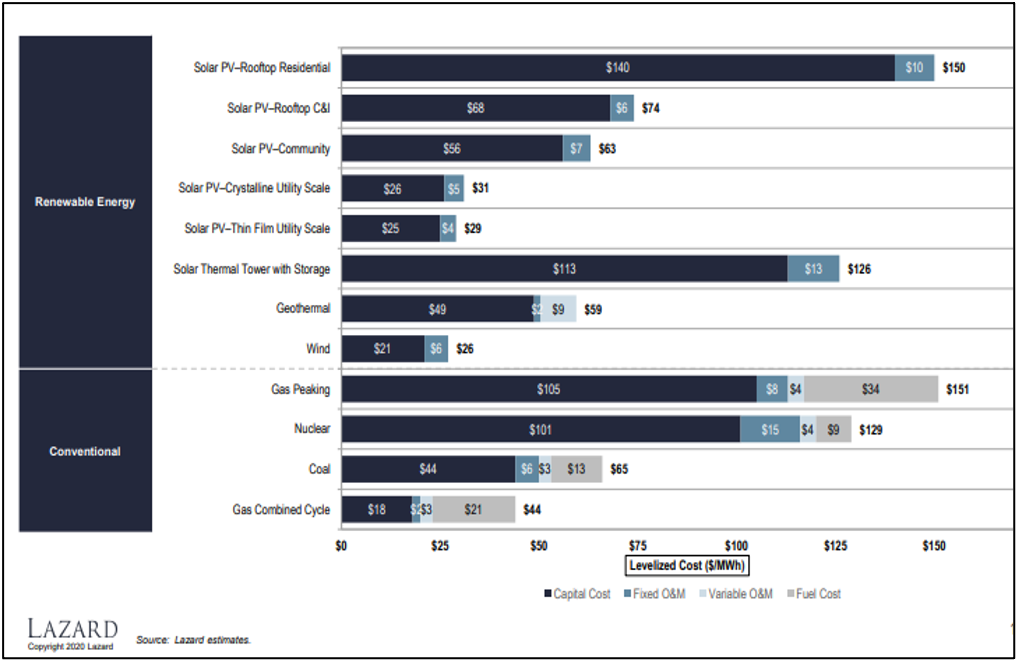

Solar PV and wind energy are the most accessible energy sources to successfully face the challenge of decarbonization by 2030-2035, supported by consolidated technologies with continuous improvements in performance. And, very importantly, they are now the least-cost option for power generation in many countries.

Solar PV has achieved grid parity in many regions of the world and is forecast to become even cheaper driven by the innovation in the solar cells materials and efficiency, as well as in the energy storage.

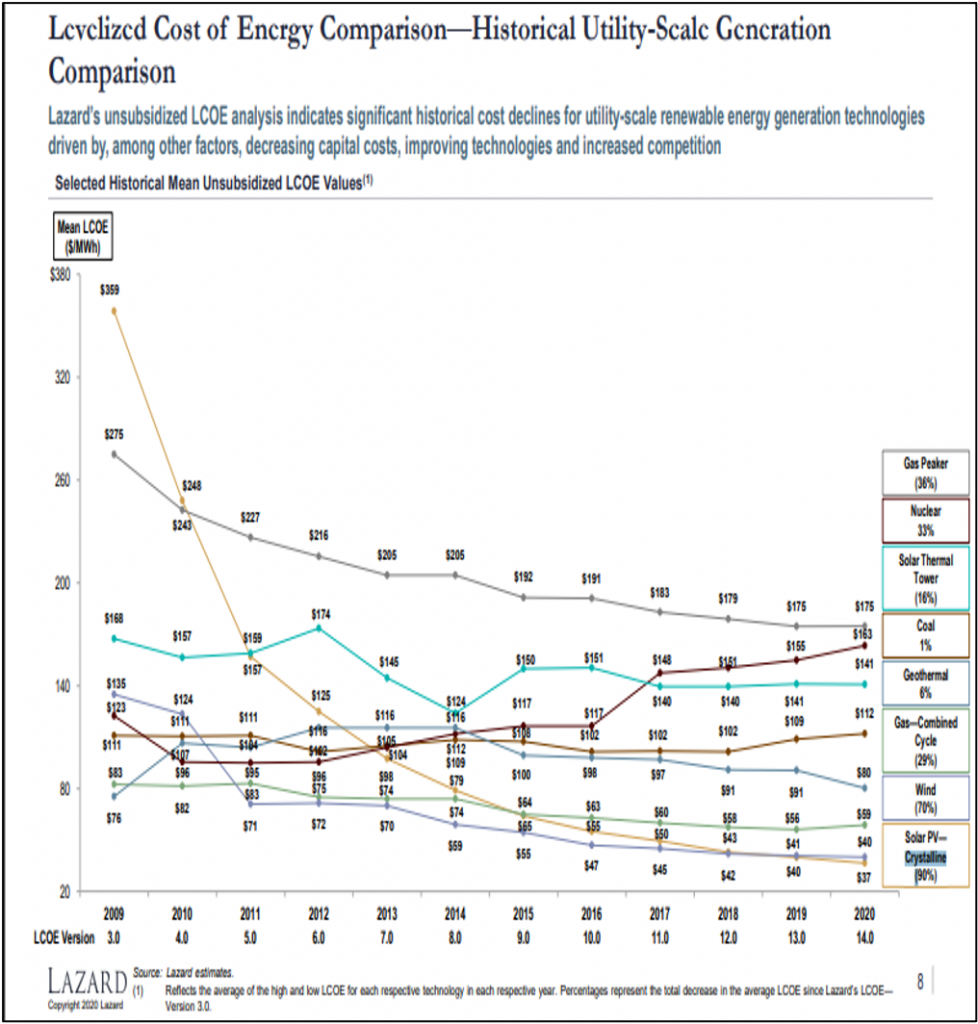

Lazard’s latest annual Levelized Cost of Energy Analysis (LCOE 14.0) shows that: the price of solar PV declined by 90% in 2010-2020, while on-shore wind energy declined by 70%.

Powering the globe

Technologies, competitiveness and maps suggest that the growth of Solar PV and Wind Energy is the feasible and most immediate response to the 2030-2035 targets challenge, as highlighted by the IEA “Renewables 2020 Analysis and forecast to 2025”.

However, it should be noted that if renewables will become the “largest source of electricity generation worldwide in 2025,” supplying one-third of global power output and accounting for 95% of the increase in total power capacity through 2025, adequate power grids capacity will be necessary.

The growth of green electricity, and the development of green hydrogen production chain itself, will require increasing and dedicated capacities in the network.

In a national context, this will be feasibile both improving the capacity for grid-side accommodation of renewable energy, as well as extending the network lines.

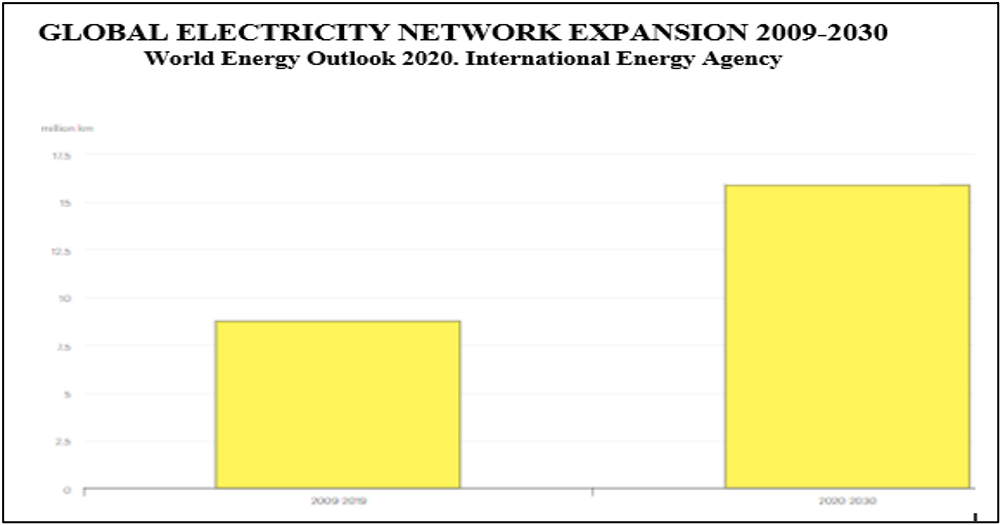

In this perspective, according to the World Energy Outlook 2020, the global electricity network will double between 2009-2030.

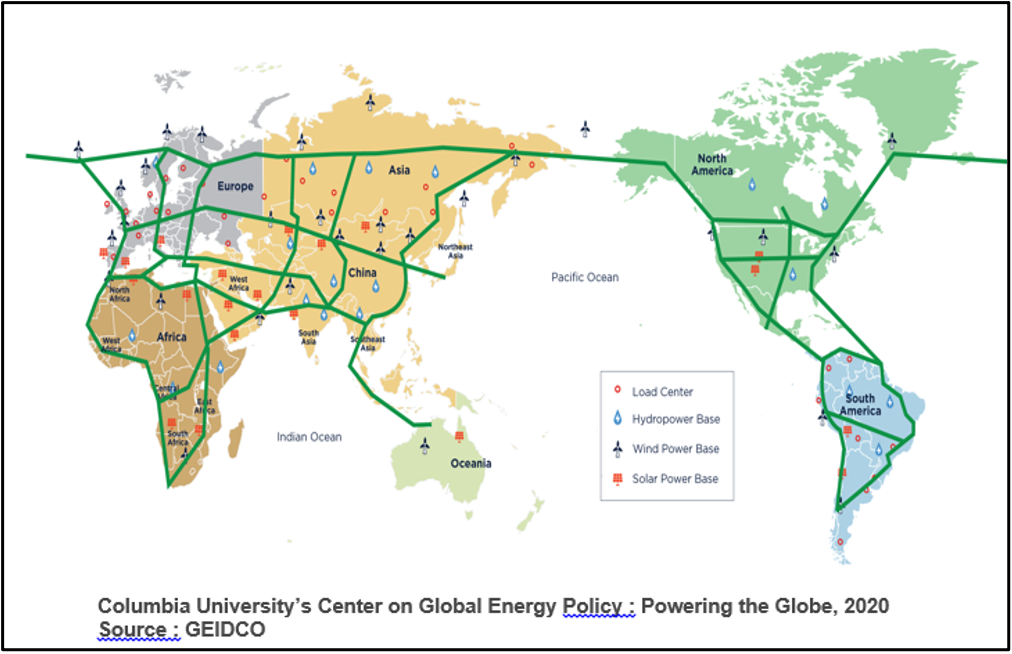

But, if we come back to the Solar and Wind Atlas, and if we look at the full exploitation of solar and wind global energy potential, the efficient transmission across continents and different time zones of electricity produced from renewable sources in remote and low-demand areas is a key driver for building in the present decade the infrastructure for the shift from fossil fuels to clean energy, as well as for balancing at global level demand and supply.

This is the vision of Global Energy Interconnection (GEI) initiative, launched by Chinese President Xi Jinping at the UN General Assembly in 2015 to “facilitate efforts to meet the global power demand with clean and green alternatives”.

We must recognize that GEI is today the most feasible option to integrate the growth of renewables with access to green electricity worldwide.

Long-distance transmission supported by Ultra High Voltage (UHV) lines “can link remote renewables to demand centers to create transnational backbone power lines. These sorts of links could help mitigate renewable supply intermittency by offering diversity of supply. Smart grid technology would enable the complex operational demands of optimizing dispatch and maintaining grid stability over these enormous areas”. (Columbia University’s Center on Global Energy Policy. Powering the globe, 2020)

Obviously we are not in the world of wonders, and the difficulties in integrating cross-border networks are known.

Technologies are available, both for the production of green electricity and for high-capacity and long-distance transmission. Technical barriers to interconnection are marginal. The barriers are political, polluted by the blunder of the decoupling of economies which, among other things, involves very high additional costs to avoid cooperation and integration.

Global responses are required to face the global challenge of climate change.

We have little time. If the 2030-2035 targets will not met, it will be very difficult to win the challenge or even simply limit the damages.

I hope that the G20 under the Italian presidency can promote a global alliance on renewables and interconnection for greening the planet.

Corrado Clini

Former chairman of G8 Task Force on Renewable Energy, and former Minister for the Environment of Italy

Show Comments